Welcome to the second video for quarterly estimates. This is step one in the spreadsheet. You'll see number two quarterly taxes and then right here step one select your tax information. So I'm gonna go line by line through this. I do recommend looking at your last year's tax return. First, you just select your filing status. Again, yellow, you enter in yellow cells throughout the spreadsheet. Everything else is calculating for you. So if you see this little arrow, that's a drop down menu. You can see your filing status on your last year's tax return. If you're not sure what it is, typically your status is based on December 31st, 2016. Were you single? Single? Were you married? Married filing joint? It doesn't matter if you got married on the 31st, you're married filing joint for the whole year. That's how your status is. And then head of household is if you are separated, you don't live with your spouse or ex all year, but you have a dependent child. And whatever you select, the amount here will automatically adjust. Now this second one, if you have your tax return in front of you, or you may know off the top of your head, if you itemize your deductions, this spreadsheet isn't set up for that. I do have spreadsheets that go with this that I sell that do your itemized as well. But if you know what that amount is, if you see it on last year's return, you can just enter it here, and the calculation will automatically incorporate that. So, but you would just have to edit and enter it there and enter it for the whole year, regardless of which quarter. Otherwise, most people don't itemize. Now, the tax people might have tricked you before and...

Award-winning PDF software

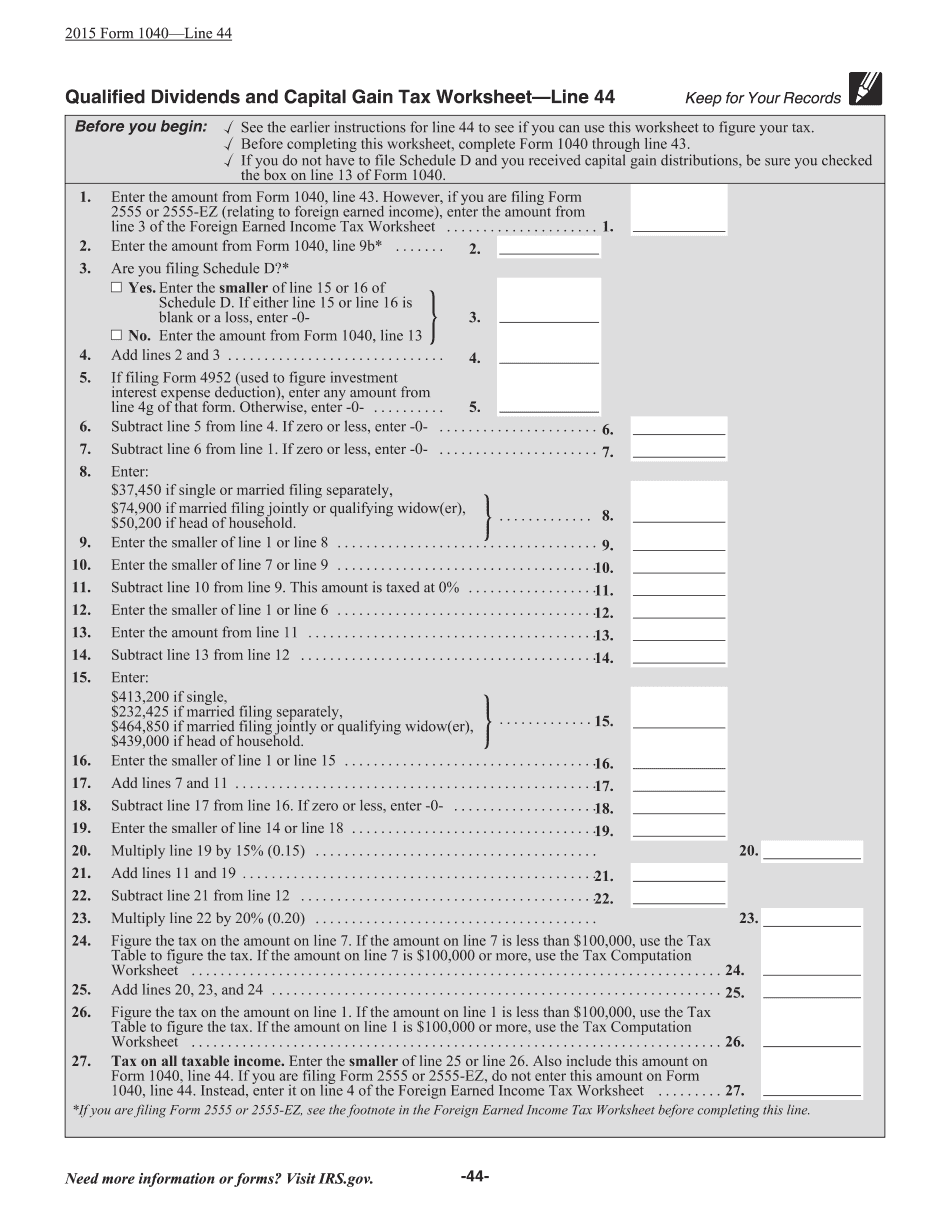

Tax computation worksheet Form: What You Should Know

Your taxable net income is less than 100,000. Tax Rate Schedule II — Use if Your taxable net income is 100,000 or more. Tax Rate Schedule III — Use if your taxable net income is less than 25,000. Tax Rate Schedule IV — Use if your taxable net income is 25,000 or more. Maryland Personal Income Tax Worksheet — Maryland Personal Income Tax Return for 2017 New York Tax Computation Schedule Use the New York tax computations worksheet(s) (Form 941-X) if your taxable net income is 100,000 or more in 2017. Tax Rate Schedule III — Use if your taxable net income is 100,000 or more. Tax Rate Schedule IV — Use if your taxable net income is less than 10,000, or your taxable net income is less than 15,000, and you are a United States citizen. Tax Rate Schedule V — Use if your taxable net income is 10,000, or your taxable net income is 15,000, or your taxable net income is less than 20,000. Tax Rate Schedule VI — Use if your taxable net income is less than 3,000, or your taxable net income is less than 4,000, and you are a United States citizen. Tax Rate Schedule VII — Use if your taxable net income is less than 1,000. New York City Tax Computation Use the New York City tax computation worksheet(s) (Form 940-X) for your year of filing and your tax year is 2017. If you use the New York City tax computation worksheet, make sure you enter the appropriate New York City tax rate and state income tax locality code. Use the table below to determine what local tax rate to use for your 2025 New York City tax. If you are making the New York City tax computation for 2017. Your state taxable income is 25,000 or more in 2017. You were living in New York City during 2017. New York City tax rates apply to 2025 federal taxable income. New York City tax rate for 2025 federal taxable income is 9,000 (9%, which is the highest rate in New York City). This rate will not apply to your 2025 federal income tax filing due date and will not be used in 2017. New York City tax rate for 2025 taxable net income. This means you earn your New York City income in New York City (and not from elsewhere).

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form instruction 1040 Line 44, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form instruction 1040 Line 44 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form instruction 1040 Line 44 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form instruction 1040 Line 44 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Tax computation worksheet